20 May 2016* - This article was written after the Financial Action Task Force Private Sector Consultative Forum, hosted by the United Nations Office on Drugs and Crime (UNODC) in Vienna between Dialogue with the Private Sector.

Conversations about anti-money laundering and counter-terrorist financing have a tendency to become somewhat repetitive and frustrating, and frequently fail to identify practical actions that might improve public-private sector partnerships. The meeting in Vienna was different, however, and this author came away with renewed optimism.

The cumulative impact of bank fines, new and scary estimates of money laundered through international financial systems, horrendous terrorist attacks and the so-called "Panama Papers", mean that anti-money laundering and counter-terrorist financing is of more interest to leaders in the public and private sector alike. Doors are perhaps starting to open.

As Je-Yoon Shin, FATF president, said in his address to the The importance of urgent action to implement FATF's measures to counter terrorist financing and help defeat ISIL in December 2015, different laws mean that one of the largest potential sources of intelligence, the banks, are often prevented from sharing information across borders within their own organisations, let alone with each other or with the authorities.

Financial intelligence offers huge opportunities and public-private sector partnerships should be playing a much more effective role in safeguarding the integrity of the international financial system and contributing to safety and security.

Banks have made an unprecedented level of investment in both people and IT. They now have significant and largely untapped expertise and financial intelligence of huge value in money laundering and terrorist financing investigations.

Unfortunately governments have yet to step up adequately to exploit this by investing in their law enforcement agencies and financial intelligence units. It has not helped that the governments have lost large numbers of their experts to the banks.

There is a dearth of people with the requisite skills to exploit this information, something which offers considerable opportunities for businesses offering training and development in this area.

Private sector forum

The meeting of the Private Sector Consultative Forum which took place in April provided a valuable insight into recent information-sharing initiatives, from obstacles to success stories. The participants, who included representatives from banks, money remitters, credit unions, e-money providers, accountants, lawyers, trust practitioners and the real estate sector, discussed the challenges they face and possible policy solutions.

These discussions may lead to the development of best practices, which may help regulators, law enforcement agencies, financial intelligence units and the regulated sector to improve information and intelligence-sharing.

Among the initiatives discussed was the development of terrorist financing indicators which would be shared by governments with their financial institutions and others to help identify and mitigate terrorist financing risks.

The meeting also covered another priority area for FATF, so called "de-risking". As banks start to implement more effective controls in response to regulatory and enforcement action, the cost of compliance is rising. In the context of the wider criticism the banks have received and regulatory reforms following the financial crisis, banks are understandably more risk-averse and concerned about their reputations.

Customers offering low returns and presenting any significant level of risk, continue to be "exited". This has had a substantial effect on financial inclusion of vulnerable and critical communities and of businesses including charities, money remitters and fintechs and is exacerbating the very risks that the international community is trying to mitigate.

This is why "de-risking" remains a priority for FATF. Pushing customers back into the cash economy makes it more difficult to track money flows and significantly raises the risk of money laundering and terrorist financing.

FATF has issued FATF takes action to tackle de-risking about this as well as comprehensive guidance on the application of the risk-based approach for banks and money remitters.

It is now working on guidance to encourage regulators to clarify their expectations of banks when managing relationships with correspondents, including in relation to conducting due diligence on customer's customers.

The forum also provided valuable insight into the experiences and challenges faced by financial institutions when entering and managing correspondent banking relationships. This will inform the development of FATF guidance which, in conjunction with work being done by the CPMI and Basel under the coordination of the Financial Stability Board, is intended to help address some of the causes of de-risking.

This is, however, a deeply complex issue, and one which has multiple causes quite apart from the way in which AML/CFT requirements are being implemented. There is unlikely to be any substantial change in behaviour in the short term.

That said, as the investment that banks are making in people and IT starts to pay off, their confidence and their regulator’s confidence in being able to manage risk will increase and in the medium to long term banks may well begin to take back many of these customers.

Consolidated strategy to combat terrorist financing

Improved cooperation and information-sharing is only one of the components of the which was developed and agreed by countries in Paris in February.

FATF will continue to research and deepen its understanding of terrorist financing risks. The development of effective measures to mitigate these risks requires a sound understanding of the methods that terrorists employ to obtain, move and use their funds.

In December, FATF brought together operational experts from intelligence, law enforcement agencies and financial intelligence units to The Financial Action Task Force leads renewed global effort to counter terrorist financing.

Days later the FATF president an unprecedented meeting of finance ministers of the UN Security Council, which led to the adoption of Resolution 2253.

A FATF meeting with the Counter ISIL Financing Group in February brought together 55 states and multilateral organisations, including the United Nations, the Egmont Group of Financial Intelligence Units, the International Monetary Fund, the World Bank and Interpol.

Earlier this month a Joint UN/FATF open briefing on depriving terrorist groups of sources of funding provided another opportunity international organisations to update and share their collective understanding of new and emerging terrorism-financing risks.

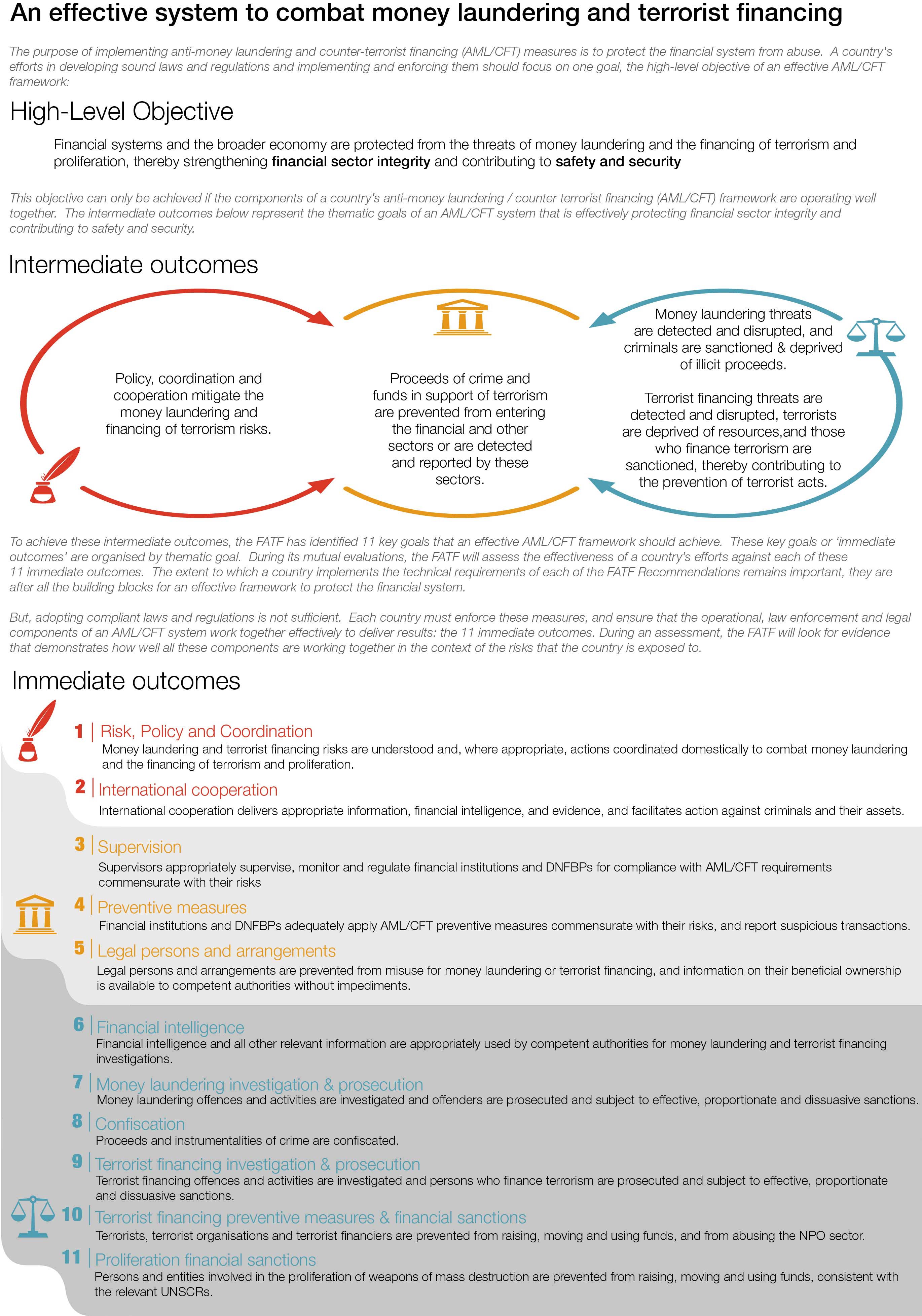

An effective system to combat money laundering and terrorist financing of FATF standards has never been more important, but, that does not mean FATF will not continue to review and revise its recommendations as necessary.

FATF strengthened the standards in October 2015 to require countries to criminalise the funding of travel for foreign terrorist fighters. It is also consulting on changing the standard intended to protect non-profit organisations at risk from terrorist financing.

In the meantime, FATF continues to identify weaknesses and loopholes in the global financial system and to hold countries to account for strategic deficiencies. It regularly reports to the G20 on the progress countries are making to address these weaknesses and to close those loopholes.

FATF's practice of naming and shaming high-risk or non-cooperative jurisdictions has proven hugely effective in forcing action. Since 2007, FATF has reviewed more than 80 countries, and has publicly listed 59 of them, leading to 43 taking substantial action to address the deficiencies identified.

The latest of these was Panama where, well before the emergence of the Panama Papers, FATF had identified failings and worked with Panama to take action. This has included the introduction in the last 12 months of new requirements on banks to identify the beneficial ownership of their customers and the regulation of lawyers, accountants and real estate firms.

A targeted review by FATF of 194 jurisdictions last year resulted in 36 countries strengthening laws and regulations on counter-terrorist financing and 22 countries committing to do so within six months.

It is essential, however, that these measures are implemented properly, and not only in those jurisdictions with nice beaches, but also in the leading G20 economies. As a result of FATF's efforts, 198 jurisdictions have committed to implement FATF standards and to be assessed on the same basis and under international procedures operated by FATF.

Most countries have legal, regulatory and operational frameworks in place but these will only be effective if countries ensure their authorities are adequately resourced to do the job and if these laws and regulations are properly enforced.

Earlier this month the G20 asked FATF and the Organisation for Economic Cooperation and Development to work together to propose ways in which the implementation of AML/CFT and tax standards could be improved, including on the availability of beneficial ownership information.

FATF has moved beyond simply assessing whether the appropriate laws and regulations are in place, and carries out regular evaluations to make countries demonstrate that those laws and regulations are being used effectively. This work will continue.

* First published on Thomson Reuters Regulatory Intelligence on 20 May 2016

Twitter

Twitter

Facebook

Facebook

Instagram

Instagram

Linkedin

Linkedin